Time is right for the comeback of quality stocks

While the broad market is flourishing, many traditional quality stocks are being wasted. The low valuation of quality companies leads to buying opportunities, many analysts believe. History also shows that quality will come to the fore in the long run.

The stock market indexes have had an excellent year. But 2025 did not have grand cru-allure for all stocks. Many companies that we usually define as top quality were left behind. In Europe, the index of quality stocks by the index calculator MSCI reached 8.6 percent. Not bad, but the broad MSCI Europe Index did more than twice as well. The 300-share global MSCI Quality Index gained 16.5 percent last year, less than the 21.1 percent for the broad MSCI World.

On Wall Street, the return of quality companies was only one-seventh compared to loss-making tech companies. In developing countries, quality stocks lagged behind the indexes by 17 percentage points, the worst performance ever.

“The past two years, the market environment has been unfavorable for quality companies,” explains Tilo Wannow, portfolio manager at Oddo BHF Asset Management. “Investors ignored the robust companies with stable business models, high returns on invested capital and reliable cash flows. The boom was mainly driven by a handful of very large companies in AI infrastructure such as semiconductors, data centers and cloud computing.”

In addition, value stocks in banks, utilities, some highly cyclical companies and defense scored superior. Traditional quality sectors, such as healthcare, consumption or software, went through a weak phase, despite often decent figures.

In Europe, names such as consumer giant Unilever, tire maker Michelin, stock exchange operator Deutsche Börse, engineering firm Arcadis, IT group Capgemini or information specialist Wolters Kluwer did not score well. On Wall Street, 38 percent of S&P500 members ended the year in the red. Pharmaceutical giants such as Pfizer, consumer giants such as Procter & Gamble, food companies such as Campbell's and Mondelez, or rock-solid companies like consultant Accenture, among others, lost ground.

“Especially in the second half of 2025, quality stocks performed poorly against the stock market indices,” says Pieter Slegers, the founder of the popular Compounding Quality newsletter, about long-term investments in quality companies. “Since 1999, they have never fared so badly against the broad market. As a result, the appreciation of what we quality stocks say it fell by 20 percent compared to the stock market average. Investors chose a more sentiment-driven strategy, preferring risky stocks, which therefore scored well.”

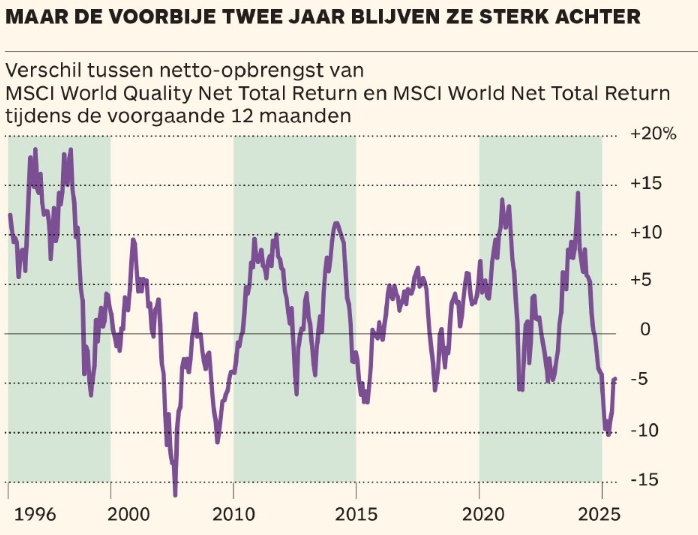

In the long term, quality stocks beat the broad market.

But over the past two years, they have lagged behind strongly.

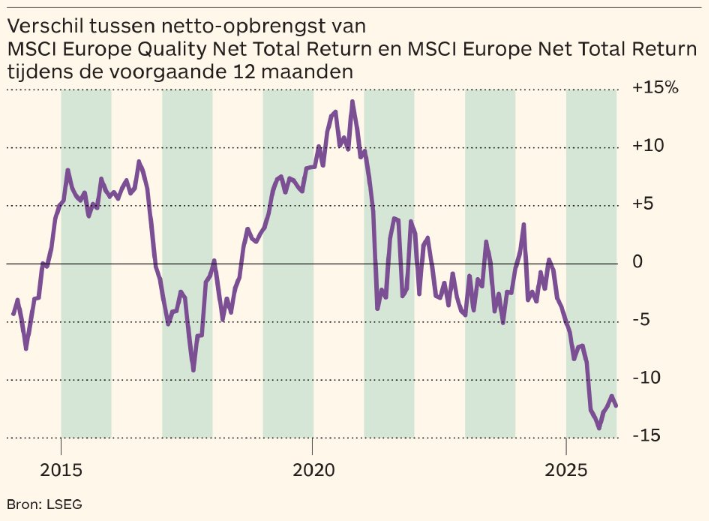

European quality stocks in particular are lagging behind

Small stocks

“The underperformance There's even more of quality in small stocks,” says Jon Eggins, chief strategist at Russell Investments. “The small, profitable companies on Wall Street have had it since Liberation Day (April 2, the day Donald Trump announced high import tariffs, ed.) done about a fifth worse than their loss-making peers in the Russell 2000 Index of small caps. This is mainly due to the sentiment among retail investors. They are looking for a short-term boom. For them, responding to a trend has become more important than fundamental criteria for choosing stocks. We call that the quality paradox. They ignore strong fundamentals in the rush to take as much risk as possible, hoping for substantial profits in the short term. '

“That's not new,” Eggins continues. “It's rooted in how markets chase cyclical movements. In “risk-on” periods (when investors take more risks, ed.) Investors often overestimate short-term profit growth and underestimate the power of stable profitability. Passive cash flows via trackers and overpopulation in some sectors with many investors holding the same positions have increased the rotation to speculative growth stocks.”

As a result, professional fund managers, who pay more attention to fundamentals, perform worse than the market. “Since April, 85 to 90 percent of active small-cap fund managers have been unable to beat the market,” emphasizes Eggins. “Not only in the US, but also in Europe and in the emerging markets.”

Part of the weaker performance of quality stocks has to do with the economic environment, Slegers explains. “The broad U.S. economy is weaker than many investors think. The growth is mainly driven by big tech and the AI boom. But many ordinary Americans are struggling. In such a climate, traditional goods producers and service providers perform weaker. '

Specifically for Europe, many European quality companies have become more dependent on the US, suggests Thorsten Winkelmann, Alliance Bernstein's chief strategist. “In Europe, many quality companies have looked outside the old continent in recent years to boost growth. The U.S. import taxes and the fall in the dollar drove many investors out of those companies in 2025.”

What is quality?

What exactly is a quality share? According to the MSCI index calculator manual, these are companies with a sustainable business model and sustainable competitive advantages. Specifically, MSCI looks at three key characteristics to include a company in one of its “Quality” indices: a high return on equity (RoE), stable profit growth that is not subject to economic cycles, and a low debt ratio. For the RoE and the debt ratio, MSCI only takes into account the last year; for profitability, the last five years.

MSCI then attaches quality scores to the stocks. There are no fixed thresholds, because they fluctuate by sector and over time. If all companies do well, the quality companies must score even better to qualify for an index seat. By using a relative score, MSCI filters out the market's highest-ranked people. Overall, a return of 15 to 20 percent on equity is very good; above 20 percent is exceptional. The debt ratio (a company's debt, expressed as a percentage of equity) should ideally remain below twice its gross operating profit (EBITDA) or half its assets, although it is highly dependent on the sector.

“Quality companies show high and consistent profitability, have strong balance sheets and experienced, disciplined management,” emphasizes Winkelmann. “Like Ryanair. The Irish budget pilot gains market share through a proven business model, enjoys much lower costs than its competitors and has a net cash position. In addition, Ryanair owns all its aircraft. His financial strength allows us to invest against the cycle. For example, during the coronavirus pandemic, Ryanair bought 300 new aircraft at a huge discount. More recently, the company invested in its own centers for the maintenance of the engines. '

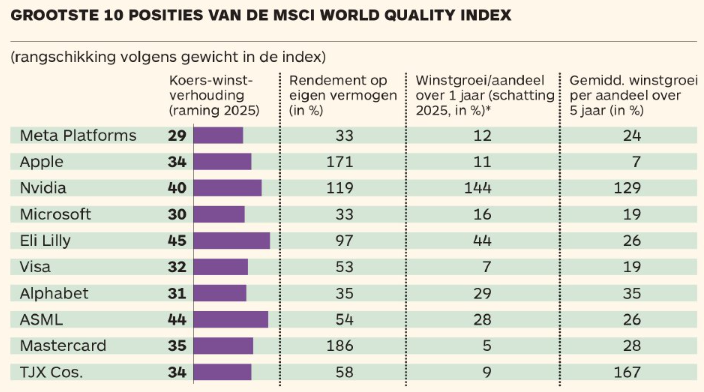

The quality stocks also include many growth companies, but only the profitable ones without too much debt. In the MSCI World Quality Index, the IT sector, weighing 29 percent, is the most important, followed by the health sector (17%), communication (13%) and industry (13%). Five of the Magnificent Seven (big tech's seven star stocks) are included in the index, except car maker Tesla and e-commerce giant Amazon. Wall Street accounts for 76 percent of the index. This is followed by Switzerland (6%), the United Kingdom (4%) and Japan (4%).

The headwinds have meant that quality companies are listing cheaply. “The S&P500 index is expensive. As a result, the expected return is barely 0 to 2 percent,” explains Slegers. “On the other hand, many quality companies are at their lowest levels in ten years. This was also the case in 1999. We all know what happened afterwards (the bursting of the dotcom bubble, ed.). For the quality companies in my portfolio, I expect annual intrinsic value growth of almost 14 percent over the next three years. In the long term, the stock price follows the intrinsic value. I'm not worried about that. '

Slegers cites the Danish pharmaceutical group Novo Nordisk, the Canadian holding Constellation Software, the credit card issuer Visa or the insurer Brown & Brown as examples of quality companies. “They've all had a hard time on the stock market, but they are rock-solid companies that haven't been so cheap in ten years.”

Moat

Slegers emphasizes that the 'moat', the moat that gives the company its competitive advantages, must remain intact. “For quality investors, that question is vitally important. The world is constantly changing. You have to ask yourself whether companies can stay just as strong in that new world. For example, there is a lot of concern whether the business models of information specialists such as Wolters Kluwer and Relx, or software companies like Adobe, will survive in the AI world. Honestly, it's still too early to say that. But the market has already severely punished such stocks, while the results remain strong for now. '

In the past, a similar neglect of quality stocks has usually been a buying opportunity. “When markets are chasing excitement, they undervalue endurance. Quality stocks have proven to perform best over the cycles,” explains Eggins. “They perform best when investors pay the least attention to them. As the candy gets sorted, we expect investors to rediscover the value of what they actually already know: quality piles up quietly, and then suddenly everyone wants it. The current gap between price and fundamentals is an opportunity to make a stronger bet on it. '

A study by Charlotte Ryland, Joseph Hawkes and Frank Mampaey, researchers at London's CFA Institute, proves that quality always comes first. They studied the performance of the various stock categories since 1998, and the longer you wait, the more the MSCI Quality Index has outclassed the global index over the past decades. Since 1998, the MSCI World Quality Index has yielded 769 percent, compared to 501 percent for the MSCI World. On a ten-year horizon, quality stocks score better in 85 percent of the periods.

Their decision? “Some star investors claim they can time the stock market. But the evidence shows that trying to time the market usually ends in poor returns. If you look at the long-term data, quality stocks have performed better than any other type of stock. '

Quality companies also offer more protection during crises. “Their prices then decline less, while they recover faster afterwards. During the financial crisis in 2008, their prices fell 30 percent and the recovery took three years. Growth stocks then plummeted more than 40 percent and took five years to recover.”

“In the past three decades, it has barely happened three times that quality stocks performed as poorly against the market average as in 2025,” says Nicolas Deblauwe, the head of the Benelux at JPMorgan Asset Management. “This makes the major dividend payers, among others, interesting. In terms of price-to-earnings, dividend stocks are almost a quarter cheaper than the broad market. '

“We see a lot of similarities with 2022,” says Mark Denham, the head of equity strategy at French asset manager Carmignac. “Even then, many top quality companies were 'oversold' and the market ignored qualitative profit growth. Afterwards, there was a rapid shift towards quality, especially from value stocks. That's why we've acquired companies such as industry suppliers Kion and Spie, the chemical distributor IMCD and building materials maker Kingspan. They are trading at very interesting valuations and combine that with strong growth prospects. In the health sector, we have strengthened positions in names such as Beiersdorf and Sartorius.”

Brussels stock exchange

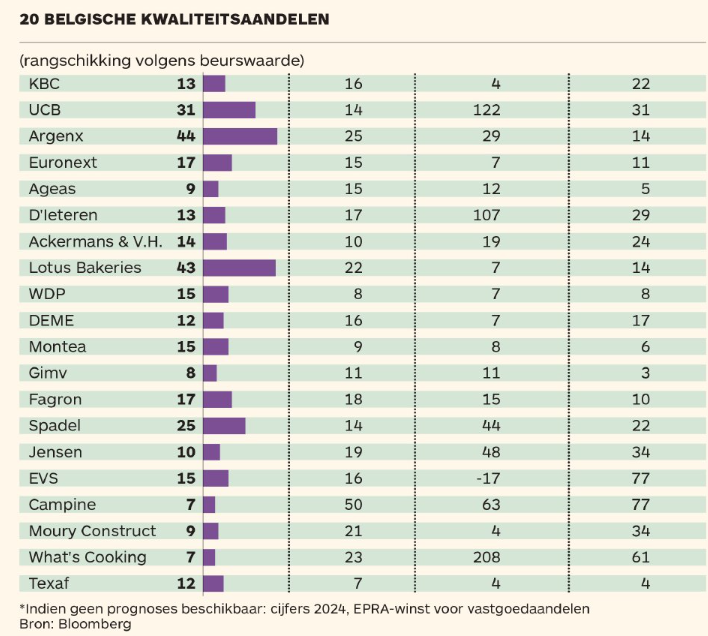

At the Brussels stock exchange, we also tried to make a selection of quality stocks. Only a handful meet all of MSCI's strict criteria, such as the pharmaceutical group UCB, the cookie maker Lotus, the insurer Ageas, the construction company Moury Construct or the maker of washing systems Jensen. That's why we occasionally added an encore to expand the list to 20 names (see table).

Some companies are too indebted to make it to the top list, such as the brewer AB InBev or the utility company Elia. The latter scores strongly on all other criteria. Moreover, the high debt ratio of seven times EBITDA (gross operating profit) is not problematic because, as a monopolist, Elia is sure of its cash flows. However, the ratio is too high to put the stock in the top 20. In real estate, companies also fell by the wayside due to the relatively high debt ratio, although they farm operationally well, such as the room landlord Xior or the retail landlord Ascencio.

In other companies, debt is not a problem and profits are growing strongly, but the return on the assets deployed is too weak to be among the top selection. This is the case, among others, with the Sipef plantation group.

The most important observation is that quality in Brussels did not perform worse than the broad market. At 19 percent, the average price climb of our twenty was the same as the profit for the Bel20 in 2025. In Brussels, it is therefore difficult to talk about a backward sector. The only notable lagging behind are Lotus and D'Ieteren, although both have been working on a strong comeback since the New Year. The restoration of quality seems to have already started on the Brussels price list.

References

- Source: De Tijd

- Link: https://www.tijd.be/markten-live/analyse/tijd-is-rijp-voor-comeback-kwaliteitsaandelen/10643885.html

- Authors: Serge Mampaey, Thomas Roelens

- Photo: Filip Ysenbaert. Historically, quality stocks are catching up after a longer period of relatively worse performance against the indexes.

- Date: 16/01/2026